The Fed's Courage To Act?

For the first time in nearly a decade, the Federal Reserve is considering raising its target interest rate, which would end a long period of near-zero rates. Like the cessation of large-scale asset purchases in October 2014, that action will be an important milestone in the unwinding of extraordinary monetary policies, adopted during my tenure as Fed chairman, to help the economy recover from a historic financial crisis. As such, it’s a good time to evaluate the results of those measures, and to consider where policy makers should go from here.Mr. Bernanke is a devastatingly brilliant economist who is promoting his new book, The Courage to Act. I agree with the thrust of his arguments above, given how dysfunctional Washington is, the Fed had to step up to the plate in 2008 to save the U.S. economy from another Great Depression.

To begin, it’s essential to be clear on what monetary policy can and cannot achieve. Fed critics sometimes argue that you can’t “print your way to prosperity,” and I agree, at least on one level. The Fed has little or no control over long-term economic fundamentals—the skills of the workforce, the energy and vision of entrepreneurs, and the pace at which new technologies are developed and adapted for commercial use.

What the Fed can do is two things: First, by mitigating recessions, monetary policy can try to ensure that the economy makes full use of its resources, especially the workforce. High unemployment is a tragedy for the jobless, but it is also costly for taxpayers, investors and anyone interested in the health of the economy. Second, by keeping inflation low and stable, the Fed can help the market-based system function better and make it easier for people to plan for the future. Considering the economic risks posed by deflation, as well as the probability that interest rates will approach zero when inflation is very low, the Fed sets an inflation target of 2%, similar to that of most other central banks around the world.

How has monetary policy scored on these two criteria? Reasonable people can disagree on whether the economy is at full employment. The 5.1% headline unemployment rate would suggest that the labor market is close to normal. Other indicators—the relatively low labor-force participation rate, the apparent lack of wage pressures, for example—indicate that there is some distance left to go.

But there is no doubt that the jobs situation is today far healthier than it was a few years ago. That improvement (as measured by the unemployment rate) has been quicker than expected by most economists, both inside and outside the Fed.

On the inflation front, various measures suggest that underlying inflation is around 1.5%. That is somewhat below the 2% target, a situation the Fed needs to remedy. But if there is a problem with inflation, it isn’t the one expected by the Fed’s critics, who repeatedly predicted that the Fed’s policies would lead to high inflation (if not hyperinflation), a collapsing dollar and surging commodity prices. None of that has happened.

It is instructive to compare recent U.S. economic performance with that of Europe, a major industrialized economy of similar size. There are many differences between the U.S. and Europe, but a critical one is that Europe’s economic orthodoxy has until recently largely blocked the use of monetary or fiscal policy to aid recovery. Economic philosophy, not feasibility, is the constraint: Greece might have limited options, but Germany and several other countries don’t. And the European Central Bank has broader monetary powers than the Fed does.

Europe’s failure to employ monetary and fiscal policy aggressively after the financial crisis is a big reason that eurozone output is today about 0.8% below its precrisis peak. In contrast, the output of the U.S. economy is 8.9% above the earlier peak—an enormous difference in performance. In November 2010, when the Fed undertook its second round of quantitative easing, German Finance Minister Wolfgang Schäuble reportedly called the action “clueless.” At the time, the unemployment rates in Europe and the U.S. were 10.2% and 9.4%, respectively. Today the U.S. jobless rate is close to 5%, while the European rate has risen to 10.9%.

Six years after the Fed, the ECB has begun an aggressive program of quantitative easing, and European fiscal policy has become less restrictive. Given those policy shifts, it isn’t surprising that the European outlook appears to be improving, though it will take years to recover the growth lost over the past few years. Meanwhile, the United Kingdom is enjoying a solid recovery, in large part because the Bank of England pursued monetary policies similar to the Fed’s in both timing and relative magnitude.

It is encouraging to see that the U.S. economy is approaching full employment with low inflation, the goals for which the Fed has been striving. That certainly doesn’t mean all is well. Jobs are being created, but overall growth is modest, reflecting subpar gains in productivity and slow labor-force growth, among other factors. The benefits of growth aren’t shared equally, and as a result many Americans have seen little improvement in living standards. These, unfortunately, aren’t problems that the Fed has the power to alleviate.

With full employment in sight, further economic growth will have to come from the supply side, primarily from increases in productivity. That means that the Fed will continue to do what it can, but monetary policy can no longer be the only game in town. Fiscal-policy makers in Congress need to step up. As a country, we need to do more to improve worker skills, foster capital investment and support research and development. Monetary policy can accomplish a lot, but, as I often said as Fed chairman, it is no panacea. New efforts both inside and outside government will be essential to sustaining U.S. growth.

But Bernanke ends his comment by stating "monetary policy can no longer be the only game in town" and here is where agree and disagree with him. In a perfect world, those politicians in Washington would all get together and pass laws by compromising on their proposals, ensuring fiscal policy would support long term growth.

Unfortunately, I just don't see this happening any time in the near future. In fact, I see the politics of division and inaction gripping Congress and the Senate becoming worse which is one reason why we're witnessing the extraordinary rise of non mainstream candidates from all sides of the political spectrum.

If someone told you we would be talking about Donald Trump, Ben Carson and Bernie Sanders as serious presidential contenders a year ago, you would have scoffed at them. Even though they don't share the same ideological views, they've been able to capitalize on the growing frustration with politics as usual in Washington.

Why am I bringing this up? Because if fiscal policy doesn't support the economy, then the only game in town by default will be monetary policy which is why Bridgewater's Ray Dalio is increasingly worried about the next downturn, and he's not the only one.

On Friday, DoubleLine Capital co-founder Jeffrey Gundlach, the current bond king, warned of 'another wave down' after the weak jobs number on Friday that the U.S. equity market as well as other risk markets including high-yield "junk" bonds face another round of selling pressure.Gundlach joins Bill Gross, the former bond king, in warning of a rout in stocks and other risk assets.

With all due respect to Ray Dalio, Jeffrey Gundlach, Bill Gross and Carl Icahn who recently warned of a looming catastrophe ahead, it remains to be seen who gets the last laugh on stocks. As I discussed in my weekend comment, with the Fed out of the way for the remainder of the year, the October surprise won't be a market crash but a huge liquidity rally in risk assets that could last well into 2016.

There is something else that happened over the weekend that received little attention as everyone was talking about Ben Bernanke's new book and how he thinks more execs should have gone to jail for causing Great Recession.

Alister Bull and Matthew Boesler of Bloomberg report, Korcherlakota Says Low Inflation Warrants Further Fed Stimulus:

Federal Reserve Bank of Minneapolis President Narayana Kocherlakota said the U.S. central bank would have been “totally justified” if it had increased policy stimulus to combat low inflation when it met last month, adding that negative interest rates could be a useful policy tool.

Speaking in an interview Sept. 29 with Arthur Levitt on Bloomberg Radio, the Fed’s most outspoken policy dove declined to say if he had recommended negative interest rates in projections submitted for the Sept. 16-17 meeting of the Federal Open Market Committee. He did say, however, that more aggressive Fed policy was warranted than the current setting of near-zero rates.

“Given the inflation outlook, given how low inflation is expected to be, to ensure the credibility of our inflation target, taking a more accommodative stance in September would have been totally justified,” Kocherlakota said in the interview, broadcast Saturday. He steps down from the Fed on Dec. 31 and is not a voting member of the FOMC this year.

The FOMC decided last month to hold rates near zero, though Chair Janet Yellen said Sept. 24 that she expected that the central bank’s first rate increase since 2006 would be warranted later this year. Kocherlakota has repeatedly argued for a delay in rate liftoff.

Accommodation TimeIn my opinion, Federal Reserve Bank of Minneapolis President Narayana Kocherlakota is way ahead of his colleagues in understanding the Fed's deflation problem. He understands the real risks of deflation coming to America and I think he has been instrumental in the sea change at the Fed which impacted its big decision to stay put on rates.

“My main point -- this is a time to think about adding accommodation, not a time to be thinking about taking it away,” he said.

Policy makers submit quarterly economic forecasts including their projections for the appropriate future path of the federal funds rate, which has been held near zero since December 2008. Displayed as dots on a chart, forecasts on the so-called “dot-plot” released Sept. 17 showed that one official viewed the appropriate rate at the end of this year and next to be slightly less than zero.

Kocherlakota said he was prevented by the Fed’s rules of confidentially from disclosing if this was his dot, though he expressed interest in the decision of central banks in Sweden and Switzerland to drive rates below zero.

“I think it’s another useful tool in our toolkit that we should be surely thinking about,” he said, in response to the question of whether the Fed should consider doing likewise if officials decided there was a need to stimulate the economy more aggressively.

“It’s been very interesting what the European central banks have been able to do in terms of actually provide more stimulus than I would have expected, by driving interest rates below what economists used to call the zero lower bound,” Kocherlakota said.

Yellen was asked about the negative dot in the Fed’s Summary of Economic Projections during a post-FOMC press conference on Sept. 17. She said “negative interest rates was not something that we considered very seriously at all today.”

Will the Fed consider negative rates any time soon? I doubt it but if inflation expectations keep sinking to record lows, this option might be considered and so will more quantitative easing (Bridgewater went on record to state more QE will come before a rate hike).

Right now, this isn't something which worries me as I believe global growth will recover in the short run, or at least that's what the stock market is indicating to me as investors bet big on a global recovery (click on image):

Is this just another countertrend rally which will fizzle out or is this part of a meaningful sector rotation back into commodities and energy following Friday's tepid jobs report? I don't know but the huge reversal on Friday may signal a change in risk appetite and you have to pay close attention to emerging markets (EEM), Chinese (FXI), Energy (XLE), Oil Services (OIH), Oil & Gas Exploration (XOP), Metals & Mining (XME) and solar (TAN) shares to see if this is part of a much bigger move.

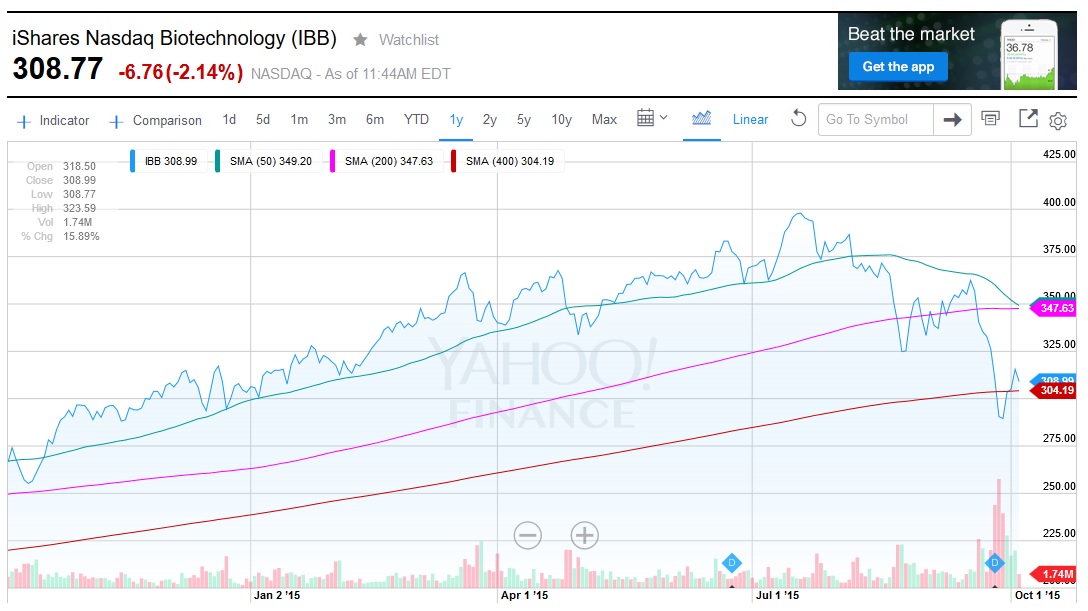

As far as large (IBB) and small (XBI) biotech ETFs, they are down late Monday morning after popping at the open but this didn't surprise me as I expected both these indexes might retest their 400-day moving average before moving back up (click on image):

A lot of traders are fretting about the "death cross" on biotech but I never took these 'death crosses' too seriously, especially in the volatile biotech sector which unlike energy and commodities is still in a secular bull market and has the potential to surge higher and make new highs.

Below, former chairman of the Federal Reserve Ben Bernanke tells USA Today's Susan Page that more corporate executives should have gone to jail for their misdeeds. Bernanke also appeared on CNBC on Monday where he stated he sees no reason why central bank policymakers should rush to increase interest rates.

I agree with him but historic low rates are fueling inequality and the buyback binge, which is very deflationary. Still, unlike Greenspan who sent out a dire warning on bonds in August, Bernanke is very cautious as he sees many risks to this tepid recovery. No wonder he's now advising Ken Griffin, the reigning king of hedge funds, the man is brilliant and very careful in his analysis.

Comments

Post a Comment